Social Security: Part 2 – Optimizing Your Benefits

Learn how Social Security works. Be confident about maximizing your benefits.

A reality check

I had a reality check when I first started as a financial advisor. People have strong opinions about Social Security. You might be thinking “duh”. But I thought it would be as simple as showing the math and voila, decision made. How naïve I was.

This big decision often comes with a lot of emotion. My goal is to bring some objectivity to the discussion by showing you how Social Security works.

In my second post of this series, let’s explore the “when should I file?” question by looking at concepts like the breakeven age, benefit increases, and longevity.

When should you file?

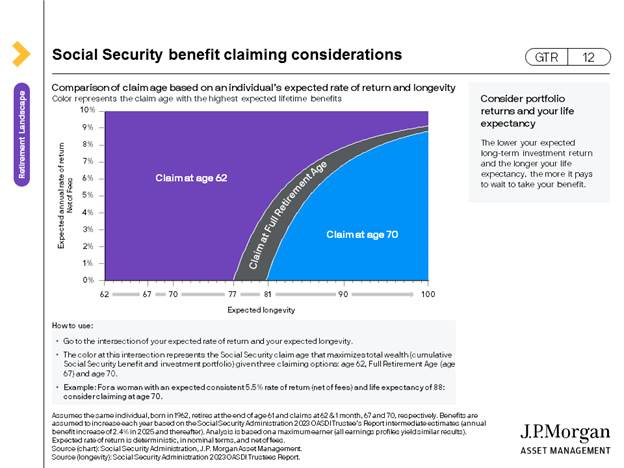

Source: JP Morgan

Breakeven age

What’s the most important variable in your filing decision? Your death. Uplifting thoughts for a Friday, right? But here’s the deal, if you did know your date of death, then you would know your optimal filing strategy.

Dying at 64? Then don’t delay until 67, take it at 62.

Planning on sticking around until 94? Then delay until 70.

This is all based on the concept of the “breakeven rate”. The breakeven age is the point at which the total benefits received from delaying equal the total benefits received by filing earlier. Beyond this age, delaying benefits results in higher cumulative lifetime payments.

The chart above is a great illustration.

If the person in the illustration expects to die by age 77, then it’s best to claim at 62. If they expect to die by age 81, it’s best to claim at FRA (66/67). If they expect to live past 81, it’s best to delay until 70.

The problem (for this exercise anyway) is you don’t know when you’ll die. That’s where probabilities come into play, which are shown at the bottom of the chart.

For example, there is a 66% probability that a 62-year-old female lives to at least age 81 – the breakeven age for filing at FRA vs. delaying until 70.

The key is to understand the facts and decide based on your unique circumstances. If you are in poor health, it may make sense to file early. If your family has a history of longevity, then it may make sense to delay.

Your benefit increases until age 70

Source: Social Security

A major component of the “breakeven rate” is the percentage increase calculation. This means the longer you wait to file, the larger your benefit will be – maxing out at age 70. (This chart applies to those born after 1960 and later)

As illustrated, if you take Social Security at age 62, you are only getting 70% of what you are entitled to – permanently reducing your personal benefit.

On the other hand, if you wait until age 70, you get 124% of your benefit - or an 8% increase every year (it’s actually calculated at .667%/month).

This increase therefore brings in another element into the equation: rate of return.

How delaying can PRESERVE your portfolio

Source: JP Morgan

“I’m taking Social Security early to protect my portfolio.” I hear this frequently. And it makes sense on the surface. But taking Social Security early can actually strain your portfolio.

Why?

The rate of Social Security increase can outpace your portfolio’s rate of return.

The chart above factors in portfolio return expectations in the equation.

Here’s the punchline: A retiree portfolio with a 4-6% return rate (a prudent assumption, in my opinion) and a life expectancy over 90 (again a prudent assumption), is best served by delaying until 70.

Here is a live example.

Delaying Until 70

File at Retirement

By delaying until 70, this couple has almost $500,000 more in their portfolio at the end of their plan.

What’s next

The key to this post is to understand the economics of Social Security benefits and how that can impact your decision to file.

In my next post, I’ll explore planning considerations for Social Security, including taxation, spousal benefits, and survivor benefits.

In the meantime, please email me your thoughts or questions!

Disclosure: All written content on this site is for information purposes only. Opinions expressed herein are solely those of Astoria Strategic Wealth, Inc. and our editorial staff. Material presented is believed to be from reliable sources; however, we make no representations as to its accuracy or completeness. All information and ideas should be discussed in detail with your individual adviser prior to implementation. Advisory services are offered by Astoria Strategic Wealth, Inc., an SEC Registered Investment Advisor. Being registered as a registered investment adviser does not imply a certain level of skill or training.

The presence of this web site shall in no way be construed or interpreted as a solicitation to sell or offer to sell investment advisory services to any residents of any State other than the State of Texas and New York or where otherwise legally permitted. All written content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. All investing involves risk including loss of principal. Past performance does not guarantee future results.

Astoria Strategic Wealth, Inc. is not affiliated with or endorsed by the Social Security Administration or any government agency.

Images and photographs are included for the sole purpose of visually enhancing the website. None of them are photographs of current or former Clients. They should not be construed as an endorsement or testimonial from any of the persons in the photograph.