What to Do with Overgrown Stock Positions (And Save on Taxes)

How donating the stock can eliminate your tax bill AND rebalance your portfolio.

Summarized Audio Transcript from the Video Above

Do you have a stock position with a hefty capital gain and you're just not sure what to do with it?

You’re not alone. I see this conundrum all the time.

Maybe the position was gifted to you. Or maybe you bought it years ago, and now it’s ballooned into a much larger part of your portfolio than you're comfortable with. And even though that's a good problem to have, it’s still a problem—especially if the position no longer aligns with your investment goals.

So what can you do?

Well, if you're charitably inclined, there’s a surprisingly elegant move that lets you continue to be generous, avoid capital gains tax, and bring your portfolio back into alignment.

Let’s walk through how this works.

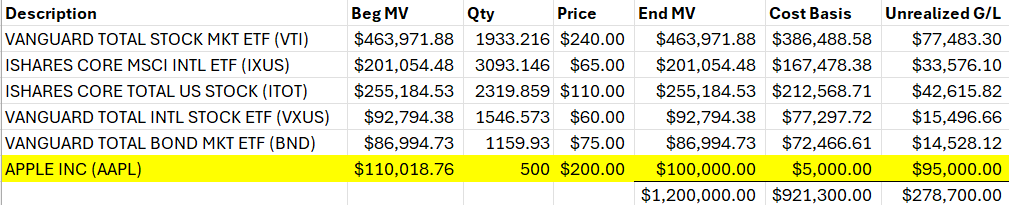

📊 A Real-World Example

Say you’ve got a fairly diversified portfolio—except for one standout position: Apple. It’s grown to $100,000, but the cost basis is only $5,000. That means you’ve got an unrealized gain of $95,000.

That kind of growth is great, but now nearly 10% of your entire portfolio is in a single stock. That’s a lot of concentrated risk for most people.

So you might be tempted to trim it back—but that $95K gain creates a new issue: a projected tax bill of $22,610 if you’re in the top long-term capital gains bracket (23.8%).

You could sell it. Pay the tax. Reinvest what’s left.

Or... you could be more strategic.

🛠️ The Donor Advised Fund Option

Let’s say you instead donate the $100K of AAPL directly to a Donor Advised Fund (DAF).

You avoid the capital gains tax entirely.

You still get a full charitable deduction.

And you’ve just positioned yourself to give generously in a more tax-smart way.

But you might be wondering: “That’s great, but now my portfolio is down $100,000.”

💡 Two Smart Ways to Replenish the Gift

Option 1: Reinvest from Cash

Let’s say you're holding $300,000 in cash between your checking and high-yield savings accounts. You go through the mental exercise:

Emergency fund? Covered.

Tax reserve? Covered.

Short-term needs like a home project or new car? Covered.

After all that, you really only need $200K in cash.

That means you’ve got room to pull $100K from cash and reinvest it—back into a diversified portfolio that aligns with your goals. Meanwhile, your DAF is funded, and your tax bill is zero on that embedded gain.

Option 2: Replenish Over Time

Let’s say you normally give $50,000 per year to charity.

By donating $100,000 in stock today, you’ve effectively front-loaded two years of giving. So for the next two years, you simply redirect that $50K/year into your portfolio instead of to your charities (because your giving is already covered).

Same generosity. Same long-term impact.

Just with better tax efficiency and better portfolio alignment.

✅ The Bottom Line

If you’re sitting on a large embedded gain and you’re also a generous person—you’ve got options.

You can:

Donate that stock directly to your Donor Advised Fund

Avoid the capital gains tax

Replenish your portfolio with cash you already have or by redirecting your future giving

It’s one of those rare win-win-win scenarios: for your portfolio, for your taxes, and for the causes you care about.

📥 Want help evaluating if this strategy could work for you?

Click here to get a free Portfolio X-Ray.

Disclosure: All written content on this site is for information purposes only. Opinions expressed herein are solely those of Astoria Strategic Wealth, Inc. and our editorial staff. Material presented is believed to be from reliable sources; however, we make no representations as to its accuracy or completeness. All information and ideas should be discussed in detail with your individual adviser prior to implementation. Advisory services are offered by Astoria Strategic Wealth, Inc., an SEC Registered Investment Advisor. Being registered as a registered investment adviser does not imply a certain level of skill or training.

The presence of this web site shall in no way be construed or interpreted as a solicitation to sell or offer to sell investment advisory services to any residents of any State other than the State of Texas and New York or where otherwise legally permitted. All written content is for information purposes only. It is not intended to provide any tax or legal advice or provide the basis for any financial decisions. All investing involves risk including loss of principal. Past performance does not guarantee future results.

Astoria Strategic Wealth, Inc. is not affiliated with or endorsed by the Social Security Administration or any government agency.

Images and photographs are included for the sole purpose of visually enhancing the website. None of them are photographs of current or former Clients. They should not be construed as an endorsement or testimonial from any of the persons in the photograph.